New Farm Bill Encourages Growers To Buy Crop Insurance

March 12, 2014

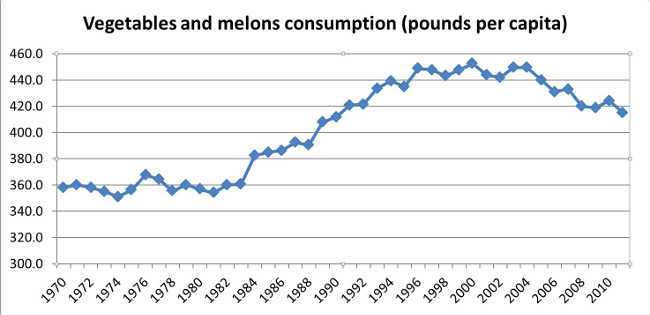

March 12, 2014 As consumer demand for fruits and vegetables increases, so do the production risks for those farmers that grow these crops. We have seen the cost of producing fruit and vegetables increase from the normal rise in inflation but also we are requiring these farmers to increase their inputs to insure the safety and security of our food supply. At the same time, we are encouraging consumers to eat more fruits and vegetables for health reasons. Higher costs are making it more difficult for some consumers to respond to that call. Note the declining per capita consumption of vegetables since 2000 (see chart). This decline is not seen as a result of consumers valuing vegetables less, it is instead evidence that higher prices and a difficult economy are making it more difficult for consumers to purchase these higher-priced vegetables.

The increasing cost of supplying vegetables also is occurring at the same time production risk is increasing for farmers. Farmers invest several thousand dollars per acre to grow some of these crops, taking on enormous risk to feed our consumers.

A Premium For Protection

The Agricultural Act of 2014 (also known as the 2014 Farm Bill) brings forth significant change to the support structure for agriculture. Direct payments made to Title I crops (e.g., corn, wheat, and soybeans) will no longer be made, and policymakers have given farmers more responsibility in managing their own risk with crop insurance programs. As USDA reminds us, insurance is intended to offer coverage needed by growers at a reasonable premium without distorting the market or affecting a grower’s management decisions for the crop. Crop insurance requires underwriting and an actuarially sound premium rate that allows premiums collected to roughly equal the indemnities paid over the long run. The Farm Bill subsidizes those premiums to encourage producers to manage risk with insurance. During some years when losses are not experienced by growers, total premiums (including the subsidy) may exceed the indemnities paid. In other years, there will be large-scale losses like those being experienced in California from the current drought or in Florida during the hurricanes of 2004. In those years, payments of claims likely exceed total premiums collected.

Safe Bet

Crop insurance is just one of the many programs supported in the 2014 Farm Bill. It helps to protect farmers from risk they cannot otherwise manage. It also helps farmers recover from unanticipated losses so that consumers have a steady supply of food. In years past, many producers of vegetables operated with the objective of breaking even on their crops four out of five years, hoping to make money in the fifth year when some other producing area suffered a crop failure. The high cost of producing these crops today and the large risks borne by these producers make it more difficult to operate like their father’s generation did. There are many ways to manage risk including knowledge of the best production practices, diversification in the crops grown, diversification in the producing regions where you plant the crops, and in the marketing programs you use to sell your crops.

Crop insurance is another way to manage risk. Crop insurance is an expense some farmers may be reluctant to make, but they should look at it as an investment for their future. An actuarially sound policy that provides premium subsidies to farmers buying those policies is an investment that will provide returns in the long run equal to the premium subsidies they receive. Looking at it another way, anyone who does not buy crop insurance is one who enjoys a high stakes game of poker.

Subscribe Today For